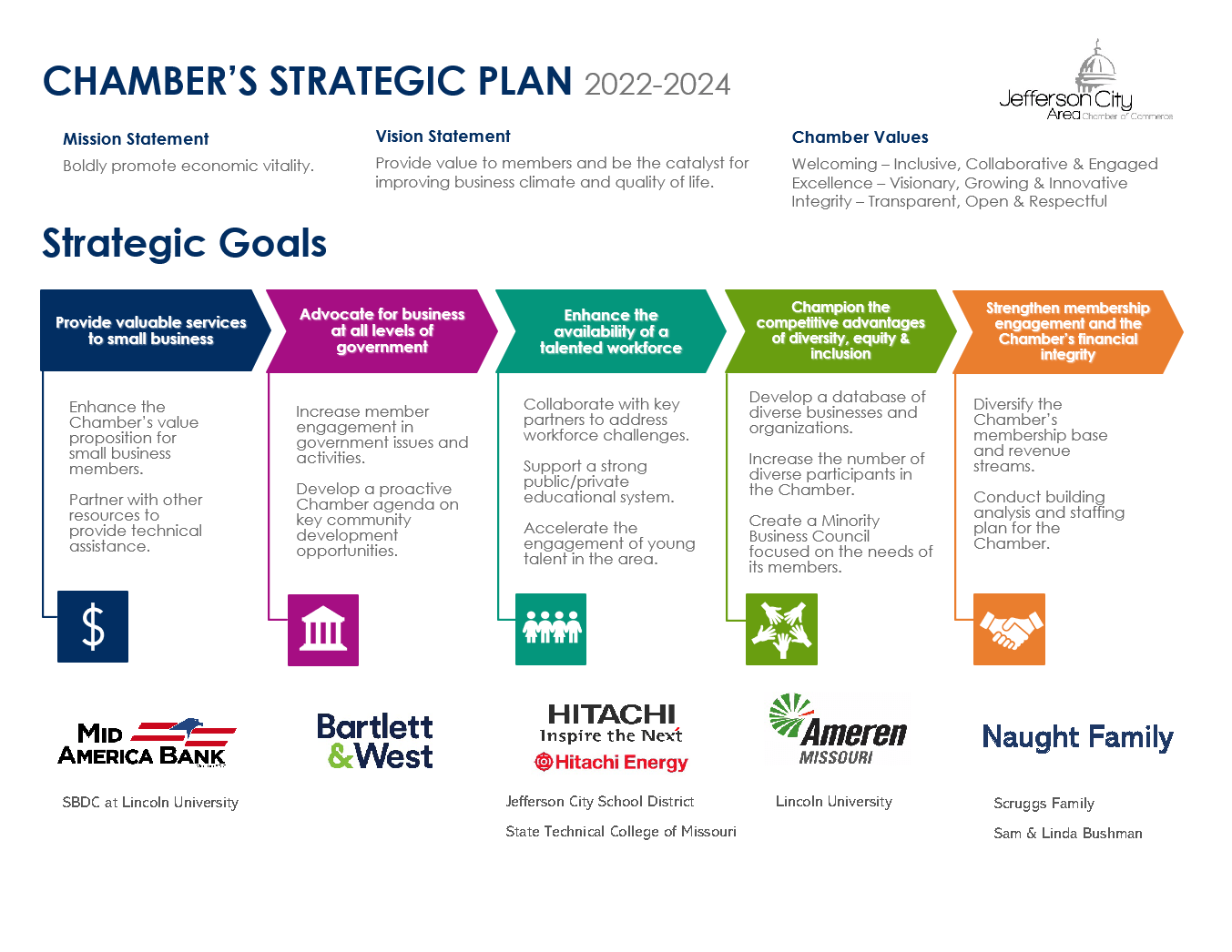

MISSION - Boldly promote economic vitality.

VISION - Provide value to members and be the catalyst for improving business climate and quality of life.

VALUES - Welcoming: Inclusive, Collaborative & Engaged; Excellence: Visionary, Growing & Innovative; Integrity: Transparent, Open & Respectful.